The underneath is an excerpt from a contemporary version of Bitcoin Mag Professional, Bitcoin Mag’s top rate markets e-newsletter. To be a few of the first to obtain those insights and different on-chain bitcoin marketplace research instantly for your inbox, subscribe now.

Core Clinical Capitulation

We’ve been highlighting the case for extra public miner capitulation over the previous few months. Information presentations that Core Clinical, the biggest publicly traded mining corporate by way of hash price and miner fleet, would possibly face chapter. The highlights from their SEC filing are the next:

- Core Clinical is halting all debt carrier bills.

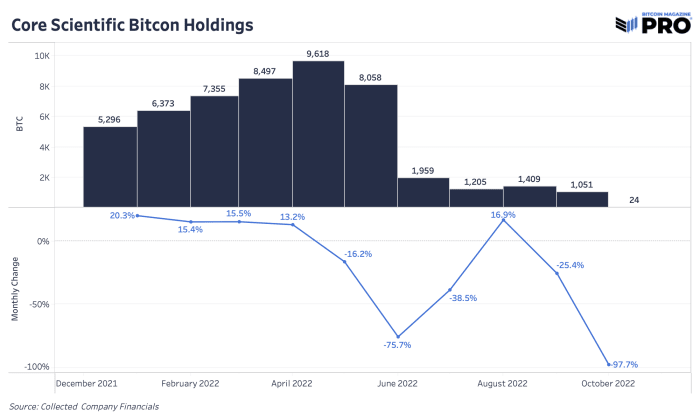

- Bitcoin holdings are actually 24; they bought 1,027 over the past month.

- Money assets will likely be depleted by way of the top of the yr or faster.

- Core Clinical claims Celsius owes them $5.four million.

An enormous within the mining area, preserving over 9,600 bitcoin at its top, Core Clinical has now just about depleted its whole treasury. Month-over-month expansion in holdings is now worse than the summer season capitulation and selloff we noticed again in June 2022. But, in June the selloff used to be a lot higher in dimension (6,099 bitcoin). It’s now not essentially the Core Clinical treasury we’re excited about now however somewhat the treasuries and holdings of all different bitcoin miners if this can be a larger take-heed call for the business.

Core Clinical’s bitcoin holdings went from a whopping 9,618 in Might to just 24 in October

Core Clinical used to be ready to power upper bitcoin manufacturing and proportion of the hash price by way of having the biggest debt-to-equity ratio within the area at 3.5. Now that debt is coming due all over the worst time to check out and lift extra fairness, with depressed costs and loss of monetary urge for food out there.

These days, the corporate’s liquidity state of affairs relies on two variables: the bitcoin value going upper and electrical energy prices coming down. Our view is that it is going to be extremely fortunate for both to materialize as a stagnating bitcoin value continues and electrical energy costs, particularly for web hosting bitcoin miners, is simplest trending upper. Having a look at Q2 profits, Core Clinical’s price of revenues went from 67% to 92% in comparison to ultimate yr. Upper energy intake prices performed a significant component.

The most important possibility related to mining equities and the emerging hash price is not just if corporations can live on and get to the opposite aspect; some will and a few received’t. Reasonably, the query you want to invite your self as an investor is whether or not your stake within the corporate gets considerably diluted alongside the best way.

For now, we expect broad-based underperformance of miners relative to bitcoin itself will also be anticipated.

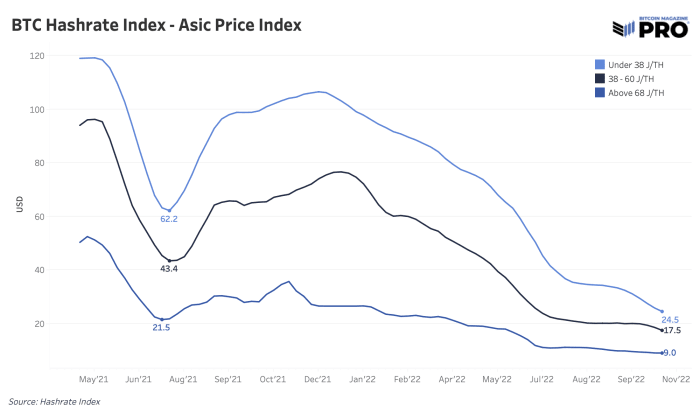

Let’s now flip our consideration to the opportunity of a capitulation around the ASIC marketplace, as Core Clinical, the sector’s biggest publicly traded mining company by way of hash price faces liquidity/solvency worries.

Even with out contemporary trends, ASIC costs had been already in fireplace sale-like territory and are at new all-time lows. Luxor’s Hash Fee Index presentations simply how depressed costs have transform throughout system potency sorts within the chart underneath. As miners have long gone to the newest, extra environment friendly rigs, that’s put additional downward value power on older mining fashions. As there’s extra call for for more recent rigs just like the S19 XP and different logo new {hardware} to stick aggressive, promoting power rises for older fashions which might be unviable or unprofitable even with the most cost effective power prices. Within the worst case, older machines are simply given away at no cost.

Even supposing Core Clinical could have many choices reminiscent of debt restructuring, Bankruptcy 11 chapter or a possible merger at the desk; promoting off and liquidating part of their 130,000 miner fleet could also be another choice. Higher promoting power by way of miners will simplest upload extra pressure to depressed costs. Additional declines in ASIC costs additionally have an effect on all miners who’re collateralizing or financing their ASICs as the worth of ASIC costs can drop additional. Now, we wait for what pressure this will likely have on hash price over the medium time period and if we’re to look a vital falloff in hash price over the following 3 to 6 months. We don’t imagine this cycle ends and not using a 20% fall in peak-to-trough hash price.

ASIC costs are in free-fall mode as hash price continues to extend whilst value remains stagnant

Ultimate word: Bitcoin mining is a brutal trade, and the present state of those stipulations is the ultimate closing endure to slay regarding the conclusion of this endure marketplace cycle and the rebirth of the following bull marketplace.

Handiest the sturdy will live on.

Related Previous Articles:

{kind=link}